| Property Tax – An Overview

Published Thursday October 8th 2009

The recent proposals

for a revision of property taxes have met with a heavy round of

criticism. Apart from the Government, there have been few supporters for

this new tax. That is not surprising since our country is entering an

economic slowdown. In terms of timing, the move was poorly judged, in my

opinion anyway. That said, I believe that a revision of our property

taxes is long overdue.

This series is

intended to provide some basic information on this important series of

questions. Most objections have been based on obvious dissatisfaction

with some government service or other. Only some of the objections have

been on the question of timing. It seems to me that the greater part of

the protest is flowing from the level of dissatisfaction with the

standard of government. That is beyond the scope of this particular

series. I have already spent most of the previous articles in Property

Matters highlighting the many strategic shortfalls which have a bearing

on the property arena.

This series is to

provide information on property tax only.

An engine of wealth

In this society,

property is both a place to live or base ones business and a means of

making money. Every successful person in the society has made a

significant part of their wealth from dealings in property; buying and

selling, fixing-up, renting-out, buying lands and cutting out lots for

sale, and so on. The taxation measures for the sector are generally very

light, which is why dealing in property is such a popular way to make

and hide great sums of money. Amidst all the recent discussion on the

pros and cons of the property tax review, we have had no real

perspectives on its place in the country’s tax revenue.

According to the

Estimates of Revenue published by the Ministry of Finance, in 1995

property tax was 2.0 per cent of tax revenue and in 2009 it was expected

to be a mere 0.18 per cent. Proportionally speaking, property tax is now

less than one-tenth the size it contributed 15 years ago. Even when one

takes into account the predicted increase in property taxes to $325

million in 2010, the proportion contributed by this source is expected

to be 1.06 per cent of the whole tax revenue. Now, while this dramatic

decline in its proportions is also due to the immense increase in the

size of other types of tax revenues, there are other aspects which are

revealed on a closer examination. When one considers the immense stores

of wealth which are held in property, beyond the basic family home, it

is sobering to realise how little the sector contributes to tax

revenues.

Modes of Property Tax

There are four modes

in which property is taxed in a modern system:

1. Stamp duty or

transfer tax: This the tax paid by the purchaser when acquiring a

property. This is the only one of the four types of property tax which

is working to some extent. Most lucrative property investments are

nowadays held in company names so that they can be split and sold by

transfers of shares, which attracts a fraction of the stamp duty payable

on a sale of property. More on that later.

2. Occupation tax:

This is the tax paid for the length of time one owns or occupies the

property and this is the one being revised now. It is called either land

& building taxes or house rates under our laws. This is not working at

all in our country and more figures will be presented in support of that

point.

3. Income tax on

rental income: This is taxes payable on the income received from

property rentals. This is poorly monitored at present.

4. Capital gains tax:

This is a tax paid on the profits made when property is sold. CGT is

only payable here in the cases of property disposals taking place within

12 months of acquisition. Few vendors dispose of property within that

time-limit.

T&T Revenue Authority

The TTRA was launched

in June 2009 and is intended to be a unified body to collect taxes and

customs duties. The Board of Inland Revenue and the Customs and Excise

Division are to be merged. Some of the cited benefits of the TTRA model

are improved revenue generation and compliance with the country’s

revenue laws; better services to taxpayers and traders; a more

professional staff complement; an improved retention of qualified

personnel; and, an improved capacity to deal with corruption. Those are

objectives with which we fully agree and the property tax review under

discussion must be understood as a part of the transition to the TTRA.

There are substantial challenges for the TTRA in this area and we will

be pointing these out in this series. As a conclusion to this readers

should consider the actual amounts earned by Land & Building Taxes

according to the official figures.

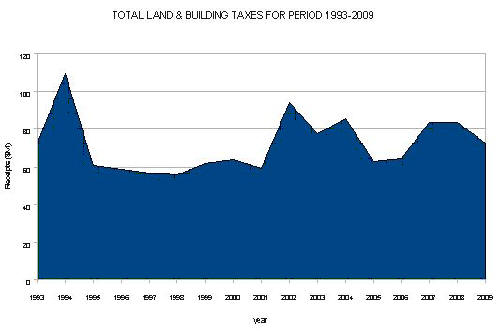

Land & Building Taxes

receipts

Year Receipts ($M)

1993 72.04

1994 109.38

1995 60.89

1996 58.64

1997 56.63

1998 55.78

1999 61.56

2000 63.90

2001 59.11

2002 94.08

2003 77.50

2004 85.54

2005 62.68

2006 64.35

2007 83.72

2008 83.77

2009 72.77

2010 325.00

2009 and 2010 are estimates

Afra Raymond is Managing Director of Raymond & Pierre Limited.

Comments can be sent to

afra@raymondandpierre.com |